Excellent Guidance About House Mortgages That You Will Want To Check Out

Article writer-Pettersson SantanaMany people dream of the day they will own a home. When you purchase a home, you feel a sense of pride. Most people have to apply for a mortgage so they can afford to buy a home. There are several key facts to learn before getting a loan, and this article can be a great help.

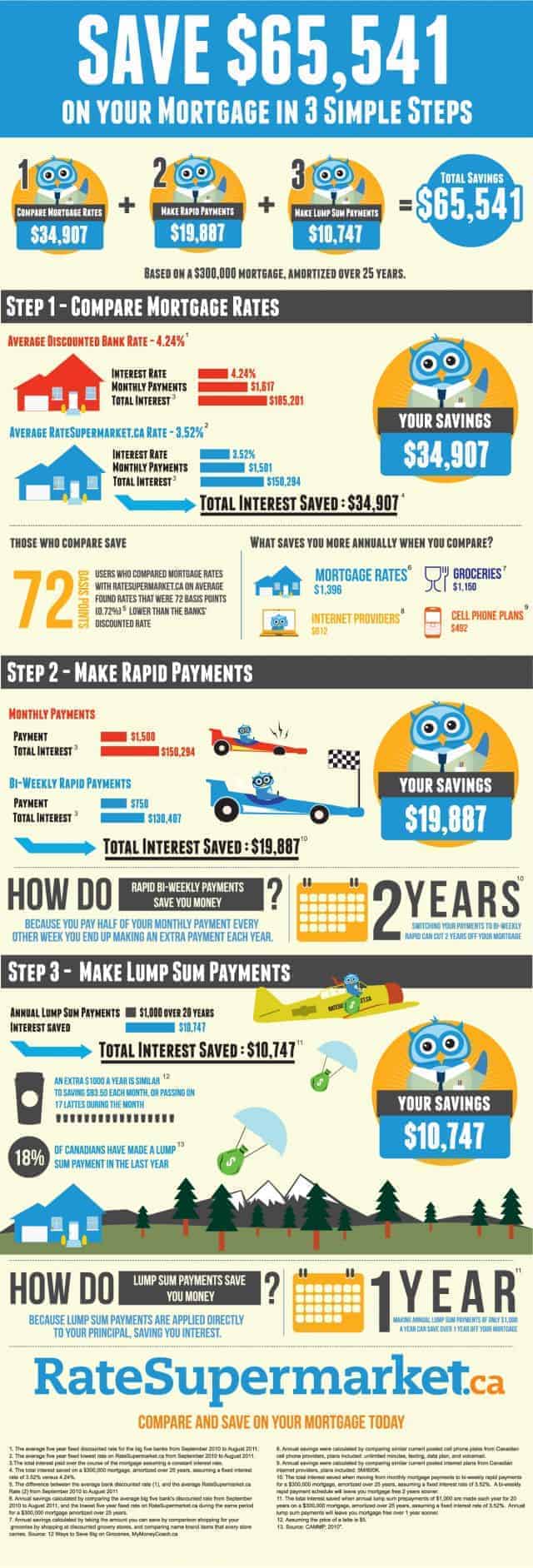

When it comes to getting a good interest rate, shop around. Each individual lender sets their interest rate based on the current market rate; however, interest rates can vary from company to company. By shopping around, you can ensure that you will be receiving the lowest interest rate currently available.

If you want to get a feel for monthly payments, pre-approval is a good start. Do some shopping to know what your eligibility looks like, so you can better estimate the price range you have. Calculating your monthly payments will be easier once you get pre-approved.

If you can afford a higher monthly payment on the house you want to buy, consider getting a shorter mortgage. Most mortgage loans are based on a 30-year term. A mortgage loan for 15 or 20 years may increase your monthly payment but you will save money in the long run.

Consider a mortgage broker instead of a bank, especially if you have less than perfect credit. Unlike banks, mortgage brokers have a variety of sources in which to get your loan approved. Additionally, many times mortgage brokers can get you a better interest rate than you can receive from a traditional bank.

Really think about the amount of house that you can really afford. Banks will give you pre-approved home mortgages if you'd like, but there may be other considerations that the bank isn't thinking of. Do you have future education needs? Are there upcoming travel expenses? Consider these when looking at your total mortgage.

Get quotes from many refinancing sources, before signing on the dotted line for a new mortgage. While rates are generally consistent, lenders are often open to negotiations, and you can get a better deal by going with one over another. Shop around and tell each of them what your best offer is, as one may top them all to get your business.

Save up for the costs of closing. Though you should already be saving for your down payment, you should also save to pay the closing costs. They are the costs associated with the paperwork transactions, and the actual transfer of the home to you. If you do not save, you may find yourself faced with thousands of dollars due.

Do not change financial institutions or move any money while you are in the process of getting a loan approved. If there are large deposits and/or money is being moved around a lot, the lender will have a lot of questions about that. If you don't have a solid reason for it, you may end up getting your loan denied.

If you have previously been a renter where maintenance was included in the rent, remember to include it in your budget calculations as a homeowner. A good rule of thumb is to dedicate one, two or even three perecent of the home's market value annually towards maintenance. This should be enough to keep the home up over time.

Shop around when looking for a mortgage. Be certain that you shop various lenders. However, also make sure that you shop around among a number of brokers too. Doing both is the only way to make sure that you are scoring your best possible deal. Aim for comparing three to five of each.

Before you apply for a mortgage, know what you can realistically afford in terms of monthly payments. Don't assume any future rises in income; instead focus on what you can afford now. Also factor in homeowner's insurance and any neighborhood association fees that might be applicable to your budget.

A mortgage broker can be a good alternative if you are finding it hard to get a mortgage loan from a credit union or regular bank. Mortgage brokers often are able to obtain financing other lenders cannot obtain. They check out multiple lenders on your behalf and help you choose the best option.

Don't be fooled by mortgage lenders that say there are "zero costs" to you at closing. It's typically a marketing ploy. The mortgage company places those funds either into the loan itself, or they are charging you a higher interest rate for the zero cost privilege. Either way, know that you are paying more over time.

If you can, you should avoid a home mortgage that includes a prepayment penalty clause. You may find an opportunity to refinance at a lower rate in the future, and you do not want to be held back by penalties. Be sure to keep this tip in mind as you search for the best home mortgage available.

There are times when the seller of a home will be able to give you a land contract so you can purchase the home. The seller needs to own the home outright, or owe very little on it for this to work. A land contract may need to be paid within a few years.

Set a budget prior to applying for a mortgage. If you end up being approved for more financing than you can afford, you will have some wiggle room. However, just click the next document is critical to stay within your means. Doing so could cause severe financial problems in the future.

Do not charge up your credit cards or open new accounts if you have been approved for a mortgage. Many lenders get an additional credit report on the borrower a couple of days before closing on the loan. Your credit score can be hurt by maxed-out credit cards or new lines of credit. This can lead to your loan being denied at the last minute.

Now that you are armed with the valuable information found in this article, you have a better chance of getting the financing you need. Your best option may be a short term loan that you can convert later, or a 30 year mortgage. Follow the advice in this article to find the loan that works best for you.